In 2025, you can expect home equity loan rates to fluctuate between 8.41% and potentially lower as Federal Reserve policies take effect. With forecasts indicating a possible decrease of up to 0.50% come December, this is an ideal time to assess your financial situation. Your credit score and loan-to-value (LTV) ratio will greatly influence the rates you receive. Waiting for a decrease might not yield substantial benefits, so it’s wise to compare multiple lenders. Interested in figuring out how to navigate these options more effectively? You’ll find valuable insights that can help guide your decision.

Key Takeaways

- Home equity loan rates are currently averaging 8.41%, with a potential decrease of 0.25% to 0.50% expected in December 2024.

- Federal Reserve rate cuts are influencing these lower borrowing costs, with a 98% chance of further cuts in November 2024.

- Economic stability and inflation trends will play significant roles in shaping future loan rates throughout 2025 and beyond.

- Borrowers should prioritize immediate financial needs when applying, as current rates are among the best seen in two years.

- Comparing multiple lender offers is crucial to secure competitive rates, especially considering credit score and loan-to-value ratio impacts.

01 Home Equity Loan Calculator: HEL Calculator

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Current Home Equity Loan Rates

As of November 2024, you’ll find that the average home equity loan rate sits at about 8.41%, down from 8.61% earlier this year. This decrease in home equity loan rates is largely due to the recent cuts by the Federal Reserve, which have led to lower rates across the board.

If you’re considering borrowing from your home, it’s important to compare these current rates with those of a traditional mortgage.

The average interest rate for a 30-year mortgage is around 6.88%, making home equity loans, classified as second mortgages, typically more expensive. For example, if you take out a $100,000 home equity loan, you might face an average rate of about 6.63%, resulting in monthly payments of approximately $775.

When looking at equity loans vs. first mortgages, it’s clear that while home equity loans can provide quick access to cash, they usually come with higher rates.

Understanding the nuances of current home equity loan rates will help you make informed decisions about your financing options and manage your monthly payments effectively.

home equity loan interest rate comparison

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Factors Influencing Loan Rates

Understanding the factors that influence home equity loan rates is key to making smart borrowing decisions. Several elements come into play, shaping your borrowing experience. Here’s a breakdown:

| Factor | Description | Impact on Rates |

|---|---|---|

| Federal Reserve | Changes in interest rates set by the Fed affect borrowing costs. | Rate decreases with cuts. |

| Credit Score | Your score typically needs to be between 620-680. | Higher scores yield better rates. |

| LTV Ratio | Measures equity in your home; lower LTVs lead to better offers. | Borrowing less than 85% is ideal. |

| Economic Conditions | Job market strength and inflation trends influence demand. | Stronger economy can raise rates. |

| Market Competition | The number of lenders and investor interest in mortgage-backed securities can fluctuate. | More competition usually lowers rates. |

Your understanding of these factors can help you navigate the landscape of home equity loan rates more effectively. By considering your credit score, LTV ratio, and the current economic conditions, you can position yourself to secure a favorable rate. Always keep an eye on Federal Reserve actions and market competition as well.

The Australian Guide to Buying Your First Home: How to Increase Your Income, Manage Your Mortgage and Get Debt-Free

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Future Rate Predictions

Experts frequently predict that home equity loan rates could see a decrease of 0.25% to 0.50% in the near future, largely driven by anticipated cuts from the Federal Reserve in 2024.

The CME Group FedWatch Tool shows a 98% probability of a federal funds rate cut in November 2024, which could lower HELOC rates and indirectly affect home equity loan rates.

While current rates are among the best we’ve seen in two years, waiting for further drops mightn’t provide significant benefits for borrowers.

Economic stability and inflation trends will play vital roles in shaping future rate predictions. If inflation remains low, you could see additional rate cuts in 2025, further decreasing borrowing costs for equity loans.

In this evolving environment, it’s important to stay informed about these changes.

By doing so, you can make smarter decisions about home equity borrowing. Whether you’re considering a home equity loan or a HELOC, understanding these dynamics can help you plan your financial future more effectively.

Keep an eye on economic indicators and Federal Reserve announcements to gauge how they might impact your borrowing options.

The House Hacking Strategy: How to Use Your Home to Achieve Financial Freedom

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

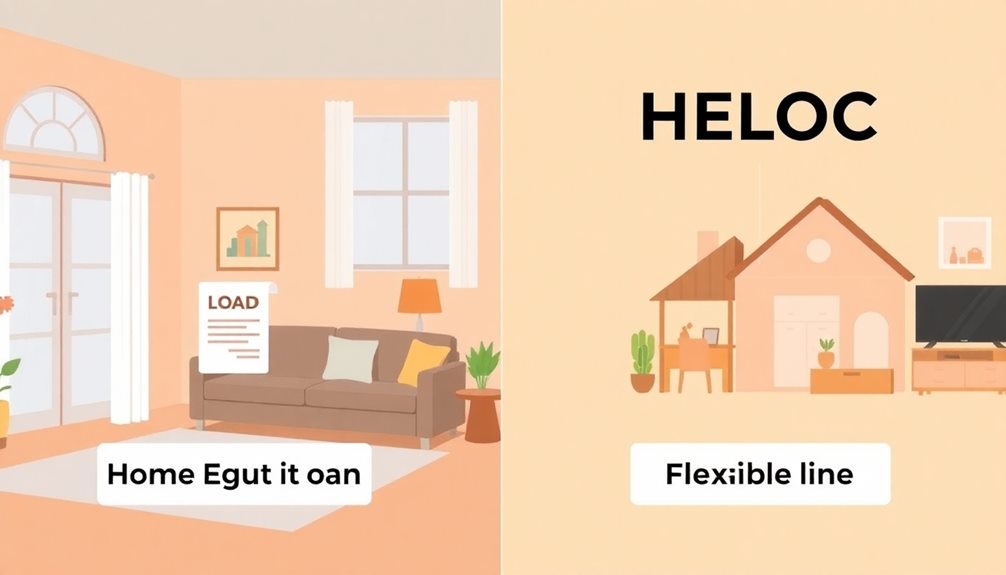

Home Equity Loan vs. HELOC

When deciding between a home equity loan and a HELOC, it’s crucial to understand how each option works and what best fits your financial situation. Home equity loans provide a fixed-rate lump sum payment, making it easier to budget for your monthly payment.

On the other hand, HELOCs offer a revolving line of credit with variable interest rates, giving you flexibility to withdraw funds as needed.

Here are three key differences to evaluate:

- Interest Rates: Home equity loans typically have higher interest rates than first mortgages, around 8.41% on average. HELOCs, however, may benefit from rate cuts if the Fed lowers rates.

- Payment Structure: Home equity loans come with a consistent monthly payment, while HELOCs can lead to fluctuating payments due to their variable interest rates.

- Financial Goals: Choose a home equity loan for large, specific projects like renovations, and a HELOC for ongoing expenses or emergencies.

Ultimately, assess your credit scores and financial goals to determine which loan option aligns best with your needs.

Timing Your Loan Application

Timing your loan application can make a significant difference in the rates you secure. As you consider your options, keep an eye on the current home equity loan rates, which are averaging around 8.41% as of November 2024.

Experts predict a potential rate cut of 0.25% to 0.50% in December, influenced by Federal Reserve policies. While this might seem enticing, it’s vital to focus on your immediate financial needs instead of solely waiting for lower rates.

Market fluctuations can impact loan pricing dramatically, so comparing multiple lender offers promptly is necessary. By acting quickly, you can secure favorable terms that align with your financial goals.

Long-term projections show minimal differences based on timing, so don’t hesitate to apply if you need funds for home improvements or debt consolidation.

Consider how different home equity products can fit into your financial strategy. While a rate cut could lower interest rates, it’s important to make sure that your loan application aligns with your current needs.

Stay informed about market trends, but remember that the best time to apply is when you’re ready to meet your financial objectives.

Economic Indicators to Watch

Understanding economic indicators is vital for maneuvering the home equity loan landscape. By keeping an eye on these key factors, you’ll be better equipped to anticipate changes in home equity loan rates and make informed decisions.

Here are three economic indicators to watch:

- Federal Reserve Policy: Changes in the federal funds rate can directly impact borrowing costs. With a 98% chance of a rate cut indicated for November 2024, it’s important to stay updated on the Fed’s decisions.

- DTI and LTV Ratios: Your debt-to-income (DTI) ratio and loan-to-value (LTV) ratio greatly affect your loan rates. Borrowers with favorable financial profiles often enjoy competitive offers, so monitor these metrics closely.

- Market Stability and Political Events: Fluctuations in market stability can affect home equity loan rates. Additionally, political events, like upcoming elections, can lead to shifts in economic conditions, influencing interest rates and borrowing trends.

Loan Options and Comparisons

How do you choose the right loan option for accessing your home equity? You have several options, each with its pros and cons. Home equity loans offer fixed interest rates, making your monthly payments predictable, while HELOCs come with variable rates that can change over time. Here’s a quick comparison:

| Loan Option | Key Features |

|---|---|

| Home Equity Loan | Fixed rates, 80-90% loan-to-value ratios |

| HELOC | Variable rates, flexible borrowing |

| Cash-Out Refinancing | Larger mortgage, changes loan terms |

| Interest Rates | Home equity loans: ~8.41% (Nov 2024) |

| Monthly Payments | Predictable for loans, variable for HELOCs |

When you’re considering borrowing, pay close attention to your credit scores, as they greatly impact the interest rates you’ll receive from home equity loan lenders. Comparison shopping is essential, as rates can vary widely among lenders. Some may offer discounts based on your qualifications or if you’re already a customer. Ultimately, understanding your options will help you make an informed decision that suits your financial needs.

Best Practices for Borrowers

When considering a home equity loan, you should prioritize your immediate financial needs and goals instead of waiting for potential rate drops. Current home equity loan rates are among the best seen in the past two years, so acting now might be beneficial.

To make the best decision, follow these best practices:

- Check Your Credit Score: A high credit score is essential for securing favorable home equity loan rates. Most lenders look for scores between 620 to 680, so aim to improve yours if needed.

- Shop Around: Don’t settle for the first offer. Compare rates and loan terms from multiple lenders to find the best home equity option for your situation. Variations in market competition can lead to significant savings.

- Consult Mortgage Professionals: Seeking advice from mortgage professionals can provide tailored insights based on your financial needs. They can help you understand the differences between fixed-rate loans and HELOCs, ensuring you make an informed choice.

Understanding Loan Terms

Home equity loans offer a valuable financial tool for homeowners looking to leverage their property’s value. Understanding the loan terms is essential before you decide to borrow against your property value. Typically, home equity loans feature fixed interest rates, which means your monthly payments will remain stable throughout the loan term, avoiding surprises if market rates change.

To qualify, you’ll generally need at least 15% to 20% equity in your home. The loan-to-value (LTV) ratio, calculated by dividing your outstanding mortgage balance by your home’s appraised value, is critical for loan approval. Repayment terms usually range from 5 to 30 years, giving you flexibility in managing your finances.

Here’s a quick overview of key factors:

| Factor | Description |

|---|---|

| Loan Amount | Up to 80%-90% of home’s appraised value |

| Equity Requirement | Minimum of 15%-20% equity needed |

| Interest Type | Fixed interest rates provide predictable payments |

| Repayment Terms | Ranges from 5 to 30 years |

| Usage of Funds | Home renovations, debt consolidation, major expenses |

Knowing these terms helps guarantee you make informed decisions about home equity loans.

Resources for Homeowners

Steering through the world of home equity loans can feel overwhelming, but plenty of resources are available to help you make informed decisions. To navigate your options effectively, consider these three key resources:

1. Online Marketplaces: Use these platforms to compare competitive home equity loan rates from multiple lenders. This way, you can find offers tailored to your financial needs.

Additionally, understanding common financial terms can help you make sense of the various loan options and their implications.

2. Guides and Educational Content: Familiarize yourself with home equity lines of credit and cash-out refinancing through various guides. Understanding these borrowing options can clarify costs and benefits.

3. Financial Newsletters: Sign up for newsletters from financial experts. They provide ongoing market updates and valuable insights, keeping you in the loop about potential rate changes.

Additionally, consulting mortgage professionals can offer tailored advice based on your specific circumstances.

Remember, maintaining a high credit score is essential for securing favorable home equity loan rates. Regularly monitor your credit and explore various financial institutions to discover the best offers available.

Frequently Asked Questions

Will Home Equity Loan Rates Go Down in 2024?

You might find home equity loan rates decreasing in 2024, but it’s crucial to reflect on your immediate financial needs. Don’t wait for potential drops; current rates are among the best seen recently. Act now!

Will Loan Interest Rates Go Down in 2024?

You might see loan interest rates decrease in 2024, especially with anticipated Federal Reserve cuts. However, it’s essential to focus on your current financial needs rather than solely waiting for potentially lower rates.

Will Home Equity Rates Go Down in 2025?

If you look at the projected 8.41% average home equity loan rate, there’s a good chance it could drop further in 2025. Monitoring economic trends will help you spot when to act for potential savings.

How Much Is a ,000 Home Equity Loan per Month?

For a $50,000 home equity loan at an average interest rate of 8.41%, you’d pay around $320.16 monthly over 20 years. Your actual payment might vary based on rate and loan terms.

Conclusion

As you navigate home equity loans in 2024, keep in mind that rates are projected to rise, with a recent survey showing that nearly 60% of homeowners plan to tap into their equity this year. By understanding the factors that influence your loan options and timing your application wisely, you can secure the best deal. Stay informed and proactive to make the most of your home’s value—it could be a game-changer for your financial future!